Says Jeff Brandes voted to allow state-run Citizens Property Insurance to dump policies onto "out-of-state, unregulated private companies."

Our only agenda is to publish the truth so you can be an informed participant in democracy.

We need your help.

A third-party group is targeting St. Petersburg Rep. Jeff Brandes.

A mailer circulating in Tampa Bay targets St. Petersburg Rep. Jeff Brandes over a vote he took on Citizens Property Insurance Corp., the state-run company that covers more Floridians than any property insurer.

Brandes is running in the Republican primary for Senate District 22 against Rep. Jim Frishe, a 12-year House member who is backed by the electioneering group that sponsored the mailer, the Committee to Protect Florida. The GOP in District 22 is one of the most closely watched in the state.

The piece features an exasperated, white-haired man at his kitchen table, his palm to his forehead, distraught over a letter he received from Citizens. Text wrapped around the image reads:

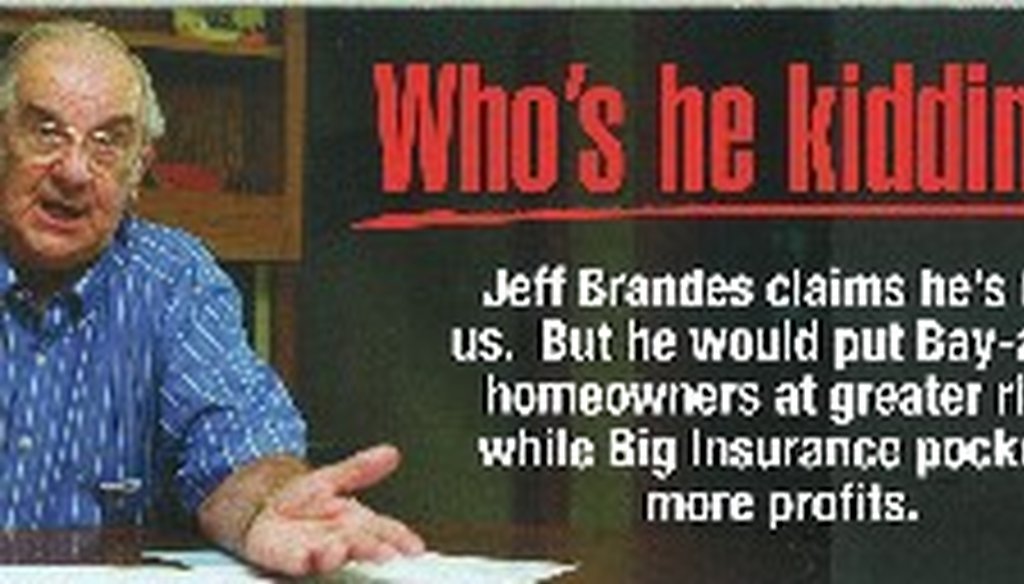

Jeff Brandes would let Citizens dump some policies...and sell out homeowners who trusted him.

Hurricanes. Sinkholes. Higher costs, weaker coverage and rejected claims.

Every Bay-area homeowner is facing big, expensive risks in today’s volatile insurance market.

Jeff Brandes wants to add another risk we can’t afford.

He voted to allow Citizens -- the state’s largest property insurer -- to dump policies onto out-of-state, unregulated private companies. Policy holders would be stuck with no control... and all the cost!

For us?

Brandes votes in Tallahassee for them. He fights for big insurance and sides with special Interests.

The fact is, with a voting record like his, Jeff Brandes is the biggest risk of all.

At hand is one of the diciest issues of the 2012 legislative session. The measure (HB 245) would have allowed "surplus lines" companies to take over Citizens policies in an effort to shrink the company. These companies, which Democrats likened to vultures, are not overseen by the state Office of Insurance Regulation and usually have higher premiums.

Many Republicans, including Gov. Rick Scott, say Citizens would be overexposed should a calamitous storm hit the state. (Read this PolitiFact Florida story for more information about the company’s financial health.)

Basically, many Republicans believe that Citizens does not have the ability to pay out claims in the event of the storm, which would leave the state in a disastrous position. So it’s better to move policyholders to other more stable companies, they say, even if it means higher premiums. They also note that Citizens was created as an insurer of last resort but has grown to be the state’s largest property insurer.

Supporters of the bill pointed to a few consumer-minded safeguards, such as requiring companies to have at least $50 million in surplus and the financial strength to withstand two hurricanes. Opponents said homeowners would be out of luck should such a company became insolvent, though, because it would not be covered by the Florida Insurance Guaranty Association.

The version that passed a full vote of the House on Feb. 3, 2012, would have automatically moved policyholders to a surplus lines company if they did not opt out within 30 days notice. (Dissatisfied customers could return to Citizens later.)

The House approved the measure 66-48. Frishe voted No; Brandes voted Yes.

That’s key to this fact-check, but there’s a little more to the story.

When the Florida Senate considered the proposal, it altered the bill be more consumer-friendly. The Senate made the measure "opt-in," meaning a consumer had to proactively approve the switch with a signature.

Supporters of the original proposal argued that the change would gut the intent of the bill: to reduce the number of policies held by Citizens. And when the amended bill bounced back to the House, Republican House members proposed to reject the opt-in provision and kick the bill back to the Senate.

But that idea failed in the the closest House vote of the session.

Both Brandes and Frishe voted against blocking the Senate’s opt-in amendment.

With the opt-in provision now part of the bill, the House sponsor said the proposal "might as well be dead" and decided not to bring it for a full vote.

Brandes, reached by phone, said he voted for the original version because "we have to take serious measures in order to reduce the exposure literally to the citizens of the state."

However, he said he was "happier" with an opt-in requirement -- which explains his vote when the bill resurfaced.

That point doesn’t matter to Roger "Rockie" Pennington, chairman of the Committee to Protect Florida, the group behind the mailer.

"When he had a chance to stand up for consumers, he stood with citizens and out-of-state, unregulated insurers," Pennington said.

Our ruling

As the ad claims, Brandes voted for a measure that would have allowed out-of-state companies to pluck Citizens policyholders in an effort to lessen Citizens’ liability in the event of a big storm.

A month later, after the Senate included a provision that would require policyholders to opt-in to the program, House members made a motion to reject that change, and Brandes voted not to reject the opt-in provision.

With the opt-in provision part of the bill, the House decided to scuttle the proposal for 2012.

The claim from the Committee to Protect Florida is accurate but needs additional information, which is our definition of Mostly True.

Florida Channel archives, Florida House debate on SB 245 (minute 165), accessed July 17, 2012

Interview with Rockie Pennington, chairman of Committee to Protect Florida, July 17, 2012

Committee to Protect Florida mailer

HB 245 vote history

Interview with Sean Shaw, leader of Policyholders of Florida, July 17, 2012

Interview with Rep. Jeff Brandes, July 17, 2012

Miami Herald, "House approves downsizing Citizens Property," Feb. 3, 2012

Miami Herald, "Amendment kills effort to reduce Citizens Insurance property holders," March 6, 2012

In a world of wild talk and fake news, help us stand up for the facts.