Says that under President Barack Obama’s health care law, "your insurance" premiums could go up by 200 percent and cost "as much as a new Explorer."

Our only agenda is to publish the truth so you can be an informed participant in democracy.

We need your help.

Former Sen. Fred Thompson, R-Tenn., tweeted that President Barack Obama's health care law will increase premiums enough to buy a new Ford Explorer. Is that correct?

As District Attorney Arthur Branch on Law & Order, former Sen. Fred Thompson was always ready with a wisecrack. In a recent Twitter post, the Tennessee Republican offered a pointed barb about President Barack Obama’s health care law:

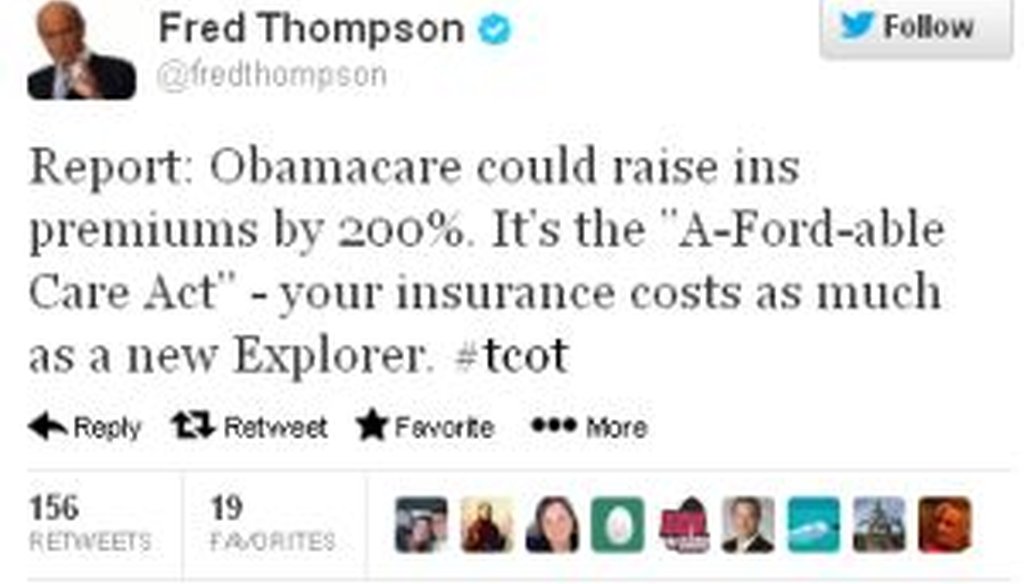

"Report: Obamacare could raise ins premiums by 200%. It's the ‘A-Ford-able Care Act’ -- your insurance costs as much as a new Explorer."

As we looked into whether Thompson’s comparison was accurate, we found a trail of facts twisted into a misleading narrative. Here’s how the tale was constructed, piece by piece.

Why premiums will go up

First, we should make clear that independent, credible experts do expect health insurance premiums to increase for many people once the mandates in the health care law take full effect, many of them in 2014.

As we have written previously, the health care law is so complex that it's difficult to predict its ultimate impact on premiums. Some parts of the law should reduce premiums (subsidies for lower-income Americans and rebates from insurers that charge too much for overhead) while other parts should increase premiums (a longer list of mandatory benefits). The overall impact will likely vary depending on your income and what type of insurance you buy.

Take special note of the "type of insurance" -- it proves to be crucial in analyzing Thompson’s claim.

There are three types of private-market insurance. Large-group plans supply coverage through an employer with more than 50 employees. Small group plans work the same way, but with the company employing fewer than 50 people. (For both types of group plans, the employees typically pay a portion of their health care premiums, and the employer pays the rest.) The third type of private insurance is in the nongroup market -- policies that people buy on their own, paying the entire cost themselves. Large group plans account for roughly 70 percent of private policies, with small-group plans accounting for about 13 percent and the nongroup market accounting for about 17 percent.

The health care law is expected to affect each of these three types of policies differently. In 2009, the Congressional Budget Office projected that by 2016, insurance premiums in the large-group market would either stay the same or drop by up to 3 percent, while the small-group market would see anywhere from a drop of 2 percent to an increase of 1 percent. The biggest rises would be felt in the nongroup market, where premiums were projected to rise by between 10 percent and 13 percent.

There’s a logic to this pattern: Currently, nongroup policies typically offer high-deductible coverage with low premiums. But under Obama’s law, all plans must provide a fixed list of benefits such as preventive care, and adding these services will come with a pricetag. So it’s reasonable for Thompson to point out that for this portion of the private-insurance market -- accounting for about one in every six private policies, many of them issued for younger and relatively healthy Americans -- will take a financial hit from the law.

The congressional Republicans’ report

We failed in our efforts to reach Thompson, but the first clue to figuring out his math is to look at the first part of his tweet: "Report: Obamacare could raise ins premiums by 200%."

We read the report, which was released in March 2013 by the Republican staffs of three congressional committees. This report is hardly a neutral document, given that it was written by staffers of a party that has worked to repeal the health care law since it was passed in 2010. Still, Thompson’s tweet goes much further than the report does, and it ignores some important qualifiers.

The Republican staff report says that "some estimates show some Americans facing startling premium increases of 203 percent because of the law."

Let’s parse this statement. First, "some estimates" refers to a January 2013 study done by former CBO director Douglas Holtz-Eakin, who served as chief economist for the Council of Economic Advisers under President George W. Bush and as a top policy adviser to the presidential campaign of Sen. John McCain, R-Ariz. His survey asked a range of companies to share premium quotes for individuals with specific demographic characteristics in five cities, before and after the health care law took effect.

In Holtz-Eakin’s study, the numbers around 200 percent refer to "young adults in the individual market" for certain cities. For instance, in Chicago, a young adult in the individual market before Obamacare would pay a premium of $756, rising to $2,268 after the law -- an increase of 202 percent. In Milwaukee, a pre-Obamacare premium of $696 would rise to $2,100, a jump of 203 percent. In three other cities listed, the increases ranged from 179 percent to 183 percent.

Looking at these figures in isolation amounts to cherry-picking. To its credit, the Republican staff report made an effort to put this number into context by listing smaller projected increases as well. For instance, when the report lists projected increases in the 50 states for all people with individual insurance -- not just "young adults" -- these premium increases range from 30 percent to 100 percent. And the Republican report cites two studies that support figures on the low end of that spectrum: The Republican report cites a study by actuarial firm Oliver Wyman that suggests increases of 40 percent in the nongroup market, while the Society of Actuaries suggests a rise of 32 percent.

These are still large increases, but they are nowhere near the eye-popping 200 percent figure that landed in headlines on conservative news sites and blogs.

And there’s an additional level of cherry picking going on as well. The Republican report looks only at the nongroup market, which, as we noted, accounts for just 17 percent of the private-insurance market. The report says nothing about the large-group and small-group markets.

This is not to say there won’t be financial hardship among young, healthy people with health insurance; there will be, and probably among other groups of Americans as well. But Thompson ignored the nuances when he tweeted that "your insurance" could rise by 200 percent. That kind of increase would only affect a vanishingly small proportion of Americans (or Thompson’s 139,000 Twitter followers).

The cost of a Ford Explorer

Some may suggest that Thompson was being facetious with his comparison, but we concluded that it's a checkable claim. And this is the part of the tweet where Thompson really goes off the rails.

According to NADAguides.com, an online auto pricing service, the manufacturer’s suggested retail price for a four-wheel drive, four-door 2013 Ford Explorer ranges from $31,995 (for the basic model) to $41,675 (for the "sport" trim). For simplicity, we’ll choose the basic model. Is there any way that health premiums will zoom past $30,000 a year as a result of Obamacare?

We can’t find any.

The people in Chicago who could be seeing a 200 percent increase in their health insurances are currently paying annual premiums of $756. After the law hits, according to Holtz-Eakin, their premiums would go up to $2,268 -- an amount well short of the $30,000 pricetag for a new Explorer.

Perhaps Thompson looked at a different chart in the Republican report. This chart, titled "Obamacare Impact on Young Adults in the Small Group Market," shows that in Milwaukee, the costs for health insurance premiums in the small-group market would rise from $28,488 before the law to $78,744 after the law. The latter amount would be enough to buy two nicely pimped up Explorers -- but it refers to the cost of premiums for a business that employs 20 people. (The Republican report’s table doesn’t explain that, but we confirmed it with Holtz-Eakin.)

Our ruling

Thompson’s tweet takes a few snippets and spins them into a misleading tale.

By some estimates, premiums for certain Americans could go up by 200 percent -- but only for a very specific type of person, namely young, healthy people who have already bought insurance on the nongroup market and will continue to do so. Meanwhile, the people who could see that big an increase would end up paying $2,200 in premiums after the law, far less than the $30,000 an actual new Explorer costs.

Thompson’s tweet illustrates what can happen when eye-catching statistics are cherry-picked and repeated without the proper context. We rate the claim False.

Fred Thompson, tweet, March 27, 2013

House Energy and Commerce Committee majority staff, Senate Committee Finance minority staff and Senate Health, Education, Labor and Pensions minority staff, "The Price of Obamacare’s Broken Promises," March 2013

Douglas Holtz-Eakin, "Insurance Premiums in 2014 and the Affordable Care Act: Survey Evidence," January 2013

Society of Actuaries, "Cost of the Future Newly Insured under the Affordable Care Act (ACA)," March 2013

Congressional Budget Office, "An Analysis of Health Insurance Premiums Under the Patient Protection and Affordable Care Act," Nov. 30, 2009

Kaiser Family Foundation/Health Research & Educational Trust, "Employer Health Benefits: 2012 Summary of Findings," accessed April 2, 2013

NADAguides.com, "New 2013 Ford Explorer Prices," accessed April 2, 2013

Email interview with Douglas Holtz-Eakin, president of the American Action Forum, April 2, 2013

Email interview with Debbee Hancock, press secretary with the House Committee on Energy and Commerce, April 2, 2013

In a world of wild talk and fake news, help us stand up for the facts.