Get PolitiFact in your inbox.

The failure of efforts to repeal and replace the Affordable Care Act has left insurance companies, states and consumers in limbo. President Donald Trump repeatedly claims Obamacare is collapsing. Supporters of the health care law say it just needs a little bit of help.

We wanted to take a step back and look at the big picture.

When federal lawmakers return to work in September, what they do on health insurance will have a direct impact on about 17 million households. Congressional action could mean the difference between affordable health care or people dropping plans that have become too expensive.

The backstory

The passage of the Affordable Care Act in 2010 brought the country closer than it ever had been to the Democrats’ goal of universal coverage. But it passed without a single Republican vote, and toppling it became a rallying cry at the same time the GOP went on an electoral winning streak. Trump campaigned on a vow to repeal and replace the law.

The law had expanded Medicaid to most poor adults. The hefty price tag was offset mainly by taxes on the wealthy and the health care industry. Republicans aimed to put a lid on spending and roll back taxes.

The law also reworked health insurance. It required that every individual have insurance; it set minimum standards that affected all plans, and it overhauled the individual market, the slice of the market for people who don’t get their insurance through their employer. That market has about 17.5 million people, or about one-ninth as many as the 156 million who are insured through employer plans.

So far, Republican efforts to repeal and replace Obamacare have fallen short. The law’s many interlocking parts proved challenging to replace without major consequences.

In an echo of the way Obamacare became law backed by one party, Republicans counted on getting rid of it without a single Democratic vote. At the end of the day, they couldn’t agree among themselves.

The latest developments

The problem right now is insurance companies are headed into 2018 without a clear idea of what the rules will be on the individual market, where people buy insurance on their own. Billions of dollars are on the line as companies get ready to lock in their rates for the coming year. The situation is shaky, and a widely shared goal is more stability.

In the Senate and the House, some Republicans and Democrats hope to cobble together a short-term fix for next year.

For the industry, the most clearly defined issues are enforcing the mandate and maintaining subsidies for lower-income policyholders.

The Trump administration, and potentially Congress, need to decide whether to enforce the mandate. The Trump administration has left this in doubt.

In terms of subsidies, the ones in play are cost-sharing payments to help lower-income policyholders cover out-of-pocket costs, for things like deductibles and co-pays. The money goes to insurance companies, and this year, the payments are worth about $7 billion to the industry. Next year, the value rises to about $10 billion.

The snag here is that in the Obama years, House Republicans successfully sued to block those payments. On appeal, a federal judge left it to the White House to decide every three months whether to cut the checks to insurance companies.

So far, the Trump administration has agreed to make those payments, but it hasn’t promised to continue. At times, Trump has hinted he would use them as a bargaining chip.

Some lawmakers would like to put Congress in charge of those payments, and guarantee them with an ongoing appropriation.

The details

Before we get to the impact of these policies, it’s important to put them into context.

Underlying health care costs continue to go up. According to the American Academy of Actuaries, insurance companies have factored in a 5 to 8 percent rise. The effect on the price tag for any particular policy depends on many things, including the local market and how the company priced a policy in 2017.

As for the role of the mandate and cost-sharing payments, the Kaiser Family Foundation, a neutral source of health care data, reviewed the preliminary rate filings of companies in 20 states and the District of Columbia. The numbers varied from state to state and company to company, but in very rough terms, each unresolved issue could add 10 percent to premiums.

In Tennessee, to take one example, Blue Cross Blue Shield added 7 percent assuming that the mandate would go unenforced and another 14 percent assuming there would be no cost-sharing payments. Together, that accounted for nearly all of the proposed premium increase.

A recent Congressional Budget Office Report projected that premiums for many plans could rise by 20 percent without cost-sharing payments.

To be sure, other things can make as much or more of a difference.

No health insurance program can escape the challenge of providing care in rural areas. With fewer providers and fewer customers, they are simply less profitable.

There’s also a divide within the individual market. Premium subsidies insulate about 8.7 million people from premium hikes. But that leaves about 6.7 million people with no subsidies who bear the full brunt of increases.

The subtext

At the most basic level, the health care debate is about the role of government and the market. Party loyalties aside, some people believe a basic level of health care is part of the social contract in the world’s largest economy. If there are families who can’t afford coverage, the government should intervene.

Others believe government actions distort the workings of the market. If Washington did less, insurance companies would be able to compete for customers. Quality would go up and prices would go down.

The Republican failure to replace Obamacare revealed a three-way split in Congress.

On one end were Republicans for whom repealing the law, something they promised to do for seven years, would be an adequate start. On the other were Democrats who see an ongoing need to support and refine the Affordable Care Act. Somewhere in between were other Republicans, including governors, with a pragmatic stance. While they would lean toward market solutions, the prospect of millions of people losing insurance or paying higher premiums was unacceptable.

Right now, the pragmatists see an opening to fix the cost-sharing problem for 2018. Sen. Lamar Alexander, R-Tenn., the chair of the Senate Health Committee said he has set his sights solely on stabilizing the individual health insurance market.

"I’m looking for the simplest bill possible that Republicans and Democrats can agree on that will stabilize the individual insurance market, so No. 1, Americans can have insurance policies to buy, and No. 2, they can afford them because the premiums stay lower," Alexander said.

The fact-checks

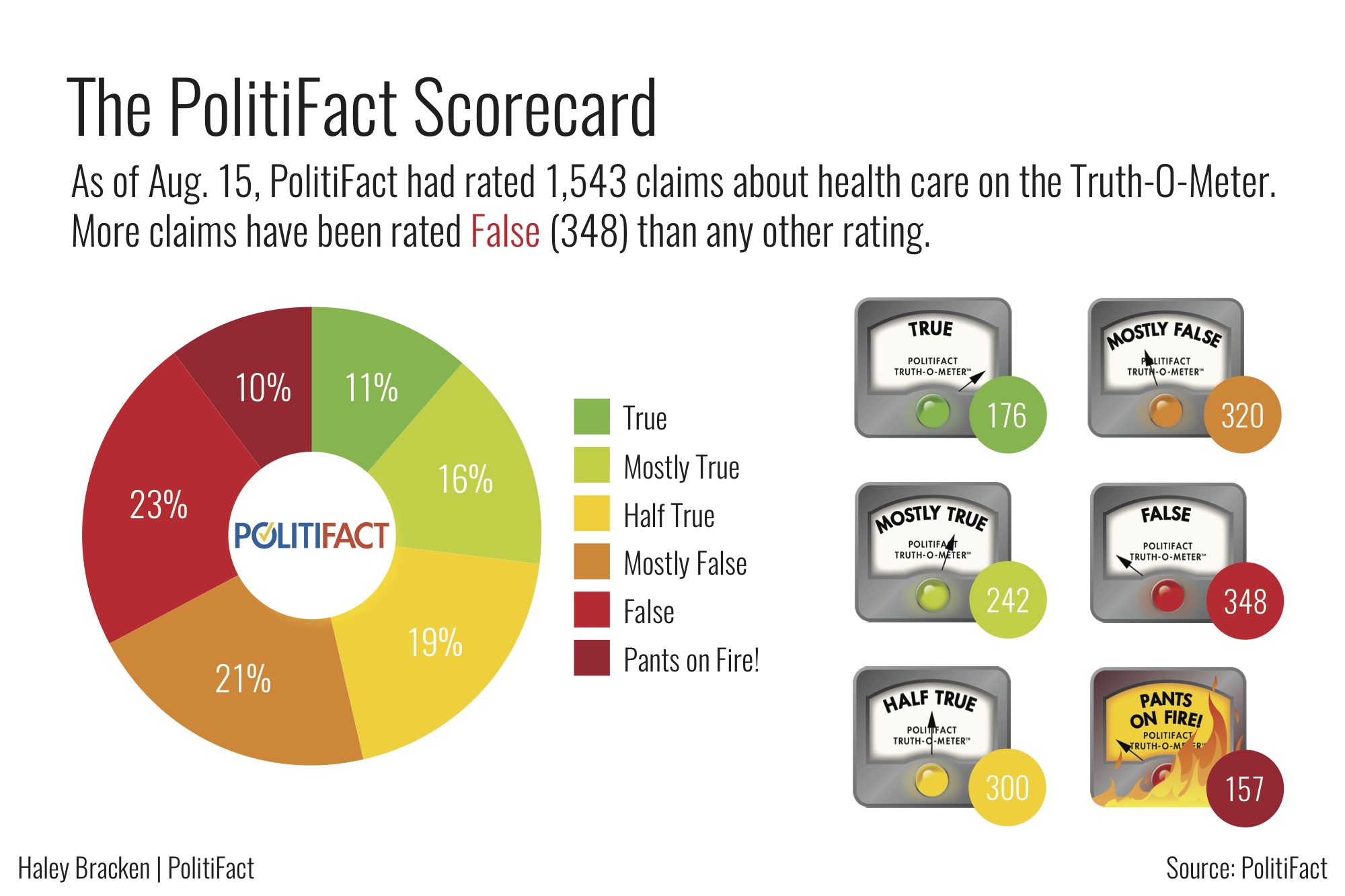

The politics in health care have always been fierce and laced with claims that fly wide of the truth. In the decade PolitiFact has been around, we’ve found that there’s about a 50/50 chance any given statement will fall into the red zone on the Truth-O-Meter.

We’ve seen many claims about insurance markets and premiums. Here’s a sample:

-

Trump said that a third of counties had just one insurer on the Obamacare exchanges (True).

-

Sen. Chris Murphy, D-Conn., said Trump had driven up premiums by not enforcing the individual mandate (Mostly False).

-

Sen. James Lankford, R-Okla., said Obamacare premiums doubled in most states this year (False).

-

Former President Barack Obama said the "vast majority" of people on the government exchanges had been spared from premium hikes. (Mostly True.)

In this divided country, these claims mirror competing economic and ideological visions. The careful reader comes to know that even when they are largely correct, they leave out part of the picture. To paraphrase Trump, health care is complicated.

PolitiFact Rating:

PolitiFact Rating:

Our Sources

Axios, The ACA stability "crisis" in perspective, Aug. 10, 2017

Kaiser Family Foundation, An Early Look at 2018 Premium Changes and Insurer Participation on ACA Exchanges, Aug. 10, 2017

Kaiser Family Foundation, Counties at Risk of Having No Insurer on the Marketplace (Exchange) in 2018, Aug. 4, 2017

American Academy of Actuaries, Drivers of 2018 Health Insurance Premium Changes, June 2017

The Hill, Senate panel to hold bipartisan hearings on healthcare, Aug. 1, 2017

U.S. Senate Health, Education, Labor and Pensions Committee, Chairman Alexander on Announcing Bipartisan Health Care Hearings, Aug. 1, 2017

PolitiFact, Is Iowa Obamacare’s canary in the coal mine? Not really., May 24

The Hill, Bipartisan group floats ObamaCare fixes, July 31, 2017

Problem Solvers Caucus, Proposal to stabilize the individual market, July 31, 2017

American Academy of Actuaries, Drivers Of 2017 Health Insurance Premium Changes, June 2016

New York Times, Republican Senator Is on a Mission to Rescue the Health Care Law, Aug. 5, 2017

Interview, Taylor Haulsee, press secretary, Lamar Alexander, Aug. 14, 2017

Interview, Helen Hare, deputy communications director, Patty Murray, Aug. 14, 2017

Congressional Budget Office, The Effects of Terminating Payments for Cost-Sharing Reductions, Aug. 15, 2017